Financial Goal Setting Checklist

A checklist for setting clear financial goals after an inheritance, helping individuals prioritize and align their financial actions.

What's Here

- Why Setting Financial Goals is Essential After an Inheritance

- Step 1: Reflect on Your Values and Priorities

- Step 2: Identify Your Short-Term, Mid-Term, and Long-Term Goals

- Step 3: Make Your Goals Specific, Measurable, and Time-Bound

- Step 4: Prioritize Your Goals Based on Importance and Urgency

- Step 5: Break Down Your Goals into Actionable Steps

- Step 6: Review and Adjust Your Goals Regularly

- Aligning Your Financial Actions with Your Goals

- Resources to Help You Stay on Track

Why Setting Financial Goals is Essential After an Inheritance

Receiving an inheritance can be a life-changing event, bringing both opportunities and challenges. While it may be tempting to splurge or make impulsive decisions, setting clear financial goals is crucial for managing your newfound wealth responsibly.

Financial goals provide direction and purpose, helping you make informed decisions about saving, investing, and spending. They can also motivate you to stay disciplined and avoid common pitfalls, such as overspending or neglecting long-term planning.

Setting goals is particularly important after an inheritance because it allows you to align your financial actions with your values and priorities. By taking the time to reflect on what matters most to you, you can create a roadmap for using your inheritance in a way that brings lasting fulfillment and security.

Remember, an inheritance is not just a financial asset – it's also an emotional one. By setting clear goals and taking purposeful action, you can honor your loved one's legacy and create a positive impact for yourself and future generations.

Step 1: Reflect on Your Values and Priorities

Before setting specific financial goals, it's important to take a step back and reflect on your values and priorities. What matters most to you in life? What kind of legacy do you want to create?

Consider questions such as:

- What are your deepest personal values? (e.g., family, security, generosity, growth)

- What experiences or achievements would bring you the greatest joy and fulfillment?

- What financial challenges or stresses do you want to alleviate for yourself and your loved ones?

- How do you want to be remembered by future generations?

Taking time for self-reflection can help you gain clarity on what you truly want to accomplish with your inheritance. It also ensures that your financial goals are grounded in your authentic values, rather than external pressures or expectations.

Be patient with yourself during this process. It's normal to have mixed emotions or competing priorities after receiving an inheritance. Trust that by staying connected to your core values, you'll find the wisdom and direction you need.

Step 2: Identify Your Short-Term, Mid-Term, and Long-Term Goals

With your values and priorities as a foundation, you can now start identifying specific financial goals. It's helpful to break these down into short-term, mid-term, and long-term timeframes.

Short-term goals (1-2 years):

- Building an emergency fund to cover 3-6 months of expenses

- Paying off high-interest debt, such as credit card balances

- Saving for a family vacation or home renovation project

Mid-term goals (3-7 years):

- Saving for a child's education expenses

- Purchasing a new home or investment property

- Starting a business or changing careers

Long-term goals (8+ years):

- Saving for a comfortable retirement

- Establishing a charitable foundation or donor-advised fund

- Providing for a child's wedding or future inheritance

Remember, your goals should be personalized to your unique situation and values. Don't feel pressured to pursue goals that don't resonate with you, even if they're common or expected.

As you brainstorm potential goals, dream big, but also be realistic. Consider your current financial situation, life stage, and any upcoming changes or challenges. Your inheritance can open up new possibilities, but it's still important to ground your goals in your actual circumstances.

Step 3: Make Your Goals Specific, Measurable, and Time-Bound

Once you have a list of potential goals, it's time to make them concrete and actionable. Vague or unrealistic goals can be demotivating, leading to frustration or abandonment down the road.

To set yourself up for success, make sure each of your goals is:

Specific: Clearly define what you want to achieve, using precise language and numbers.

- Instead of "Save for retirement," try "Save $1 million in my 401(k) and IRA accounts."

Measurable: Identify how you'll track your progress and know when you've achieved the goal.

- Instead of "Pay off debt," try "Pay off $25,000 in credit card balances and car loans."

Time-Bound: Set a realistic target date for achieving the goal, creating a sense of urgency and accountability.

- Instead of "Start a business," try "Launch my consulting business within the next 18 months."

By making your goals specific, measurable, and time-bound, you turn them from wishful thinking into a concrete action plan. This clarity will help you stay focused and motivated, even when faced with obstacles or distractions.

As you refine your goals, be sure to write them down. Putting your goals on paper (or in a digital document) makes them feel more tangible and real. It also creates a record you can refer back to as you work towards turning your dreams into reality.

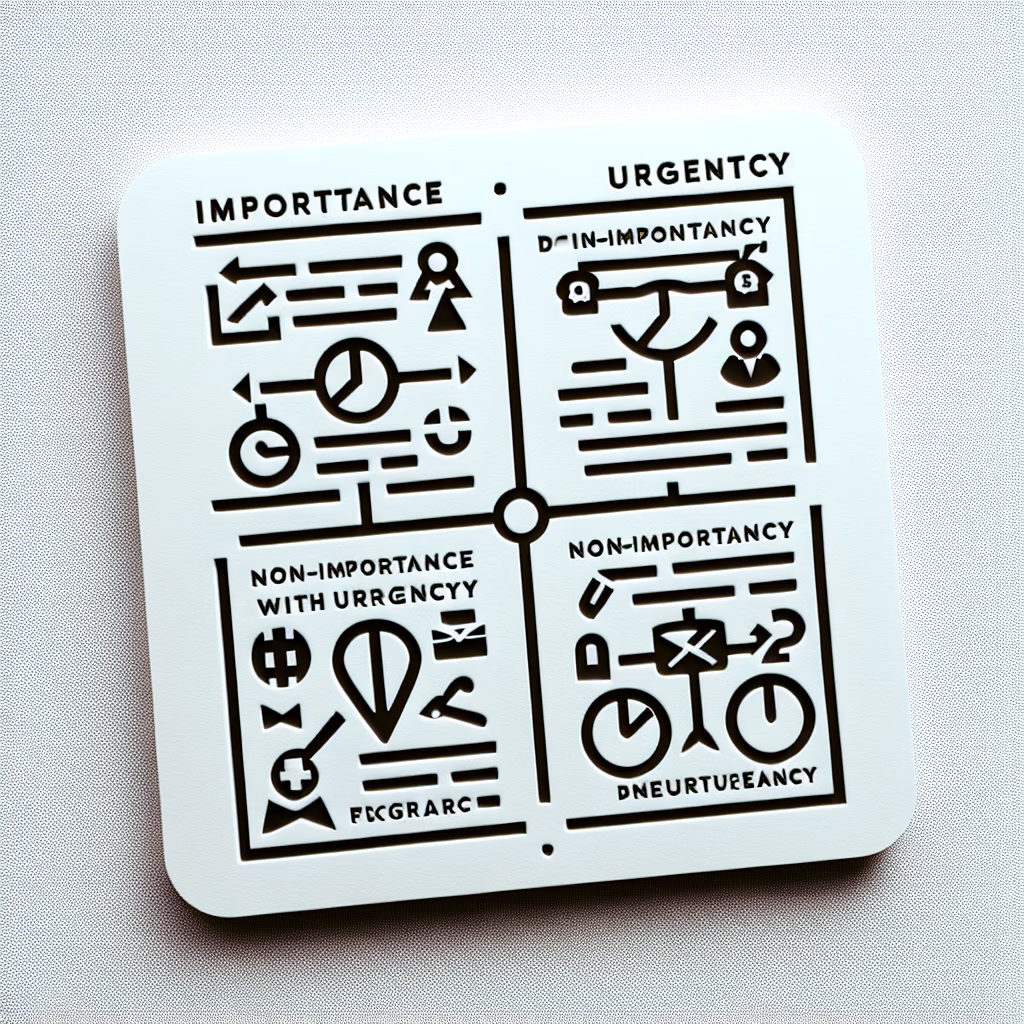

Step 4: Prioritize Your Goals Based on Importance and Urgency

After defining your specific goals, you may find that you have quite a few competing for your attention and resources. To avoid feeling overwhelmed or spreading yourself too thin, it's essential to prioritize.

One helpful framework is the Eisenhower Matrix, which helps you prioritize based on two key factors:

- Importance: How significant is this goal to your overall well-being and life satisfaction?

- Urgency: How time-sensitive is this goal? What are the consequences of delaying or not achieving it?

Using these criteria, you can categorize your goals into four quadrants:

- Important and Urgent: Top priorities to focus on immediately (e.g., building an emergency fund, paying off high-interest debt)

- Important but Not Urgent: Key long-term goals to work towards consistently (e.g., saving for retirement, establishing an estate plan)

- Not Important but Urgent: Distractions or demands to minimize or delegate (e.g., impulsive purchases, low-impact requests from others)

- Not Important and Not Urgent: Low-value activities to eliminate or avoid (e.g., mindless scrolling, procrastination)

By categorizing your goals in this way, you can better allocate your time, energy, and financial resources. Remember, you don't have to tackle everything at once. Focus on your top priorities first, while still making incremental progress on important long-term goals.

As you prioritize, be honest with yourself about what truly matters to you. Don't neglect goals that may not be urgent, but are deeply important to your values and life vision. With consistent effort over time, even small steps can lead to significant achievements.

Step 5: Break Down Your Goals into Actionable Steps

With your prioritized goals in place, it's time to translate them into a concrete action plan. Breaking big goals down into smaller, manageable steps can help you build momentum and stay on track.

For each of your top goals, identify the specific actions you need to take to make progress. These might include:

- Automating monthly savings or debt payments

- Researching investment options or working with a financial advisor

- Updating your budget to reflect new priorities

- Learning new skills or seeking mentorship to support career goals

- Communicating with family members about estate planning wishes

Be as specific as possible when outlining your action steps. Assign deadlines to create accountability, and consider any resources or support you'll need to follow through.

Remember to be realistic in your planning. While it's important to challenge yourself, trying to take on too much too quickly can lead to burnout or discouragement. Focus on consistency and incremental progress, celebrating small wins along the way.

As you take action, be prepared to encounter obstacles or setbacks. These are a normal part of the process and not a sign of failure. By anticipating potential challenges and developing contingency plans, you can stay adaptable and resilient in pursuing your goals.

Step 6: Review and Adjust Your Goals Regularly

Setting financial goals isn't a one-time event, but an ongoing process. As your life circumstances change and evolve, your goals may need to change with them.

Make a habit of reviewing your goals regularly - at least once a quarter, or whenever you experience a major life transition. During these reviews, ask yourself:

- Am I making progress on my goals as planned? If not, what obstacles or challenges do I need to address?

- Have my priorities or values shifted in a way that impacts my goals?

- Are there any new opportunities or challenges I need to consider in my planning?

- Do I need to adjust my timeline, action steps, or resource allocation to stay on track?

Be open to modifying your goals as needed based on your reviews. This isn't a sign of failure, but of growth and adaptability. As you gain new insights and experiences, your definition of success and fulfillment may change.

During your reviews, take time to celebrate your progress and successes, no matter how small. Acknowledging how far you've come can boost your motivation and self-efficacy, fueling your continued efforts.

If you find yourself consistently struggling to make progress or feeling disengaged from your goals, don't hesitate to seek outside support. Working with a financial coach, therapist, or trusted mentor can provide fresh perspective and accountability as you navigate challenges.

Aligning Your Financial Actions with Your Goals

Setting clear financial goals is a crucial first step, but true progress happens through consistent, aligned action. Every financial decision you make - from your daily spending habits to your long-term investment strategies - should support your goals.

Some key ways to align your actions with your goals include:

- Creating a budget that reflects your goal priorities, and tracking your progress regularly

- Automating savings and debt payments to ensure consistent progress

- Researching and implementing investment strategies that match your risk tolerance and time horizon

- Communicating your goals and values with family members, and involving them in financial decisions as appropriate

- Seeking ongoing education and advice to make informed, goal-aligned choices

Remember, perfection isn't the goal - progress is. There will be times when you overspend, miss a savings target, or make a decision that doesn't align with your goals. The key is to view these moments as opportunities for learning and growth, not reasons to abandon your plans altogether.

By consistently choosing actions that align with your goals - and course-correcting when needed - you'll build positive momentum and financial habits that can last a lifetime.

Resources to Help You Stay on Track

Staying focused and motivated on your financial goals can be challenging, especially as time goes on. Fortunately, there are many resources available to help you stay the course:

Financial education:

- Personal finance books, blogs, and podcasts

- Online courses and webinars

- Workshops and seminars offered by banks, credit unions, or community organizations

Professional support:

- Financial planners and investment advisors

- Accountants and tax professionals

- Estate planning attorneys

- Financial therapists or coaches

Goal-tracking tools:

- Budgeting apps and software

- Savings and investment tracking platforms

- Goal-setting journals or planners

Accountability and community:

- Joining or creating a financial support group

- Participating in online forums or social media communities

- Sharing your goals with trusted friends or family members

Remember, seeking support is a sign of strength, not weakness. By proactively accessing resources and building a network of support, you equip yourself for long-term success.

As you work towards your goals, also remember to practice self-compassion. Financial growth is a journey, with inevitable ups and downs. By staying connected to your values, celebrating your progress, and learning from your challenges, you can turn your inheritance into a powerful tool for building a fulfilling life - one aligned action at a time.